Medical Inflation in Hong Kong: Why You Become Less Able to Afford Health Insurance As You Age

On this page

- Introduction: Are You Planning for 40 Years, or 50?

- 1. What Is Medical Inflation?

- 2. How Severe Is Hong Kong's Medical Inflation?

- 3. Why Is Hong Kong Particularly Exposed?

- 4. What This Means for Your Retirement Plan

- 5. The "No-Coverage-in-Old-Age" Trap

- 6. How to Prepare: Three Reasonable Paths

- 7. Gifting Your Child a Lifetime Medical Reserve

- 8. Frequently Asked Questions (FAQ)

- 9. Further Reading

- Citations

Image: Unsplash / photographer M (@mansonyms), free to use under the Unsplash License.

Introduction: Are You Planning for 40 Years, or 50?

According to the Hong Kong Centre for Health Protection, as of 2024 the average life expectancy at birth is 82.7 years for men and 88.2 years for women — roughly 85 years overall[¹⁰]. In other words, the medical-coverage horizon facing a 35-year-old today is not the commonly-cited "until retirement at 65" (30 years), nor even "until 75" (40 years). It is 50 years or more.

More importantly, "85 years" is not a static finish line. The same CHP table shows that in 1971, Hong Kong's life expectancy at birth was 67.8 years for males and 75.3 years for females — a combined gain of roughly 15 years over the past 50-plus years[¹⁰]. Even if the rate of improvement slows to half its historical pace going forward, by the time today's 35-year-old actually reaches 75 (around 2065), Hong Kong's average life expectancy will likely stand at 88 to 90 years or higher. In other words, the finish line you're planning toward keeps moving away from you as you age into it.

That difference matters. Consider a 35-year-old non-smoker in Hong Kong who today enrols in FWD's vBooster Medical Plan (Standard ward, Asia coverage, HK$16,000 deductible — a common middle-tier setup used as a second-layer top-up on top of company medical or personal savings). According to the official premium table, the annual premium is about HK$5,736 — entirely reasonable for a year's coverage at that age.

But planning out to Hong Kong's actual life expectancy:

- At age 65 (year of retirement): HK$25,795

- At age 75: HK$42,091

- At age 85: HK$57,966

That is roughly a 10x climb over 50 years. The crucial point: stopping the projection at age 75 undercounts by exactly one decade — the decade where the premium curve becomes vertical. From HK$42,091 at 75 to HK$57,966 at 85, the age-band step alone adds nearly HK$16,000, before any medical-inflation repricing.

This climb comes purely from one factor — age. Adjusting premiums by age band is standard practice across all VHIS-certified plans. And as underlying medical costs themselves rise, insurers periodically reprice the entire premium table. In other words, the age-85 premium 50 years from today will not be HK$57,966 — it will be a higher figure inflated by five decades of medical cost growth.

This article aims to help readers understand what medical inflation is, how severe Hong Kong's situation is, what it means for retirement planning, and how to start preparing today.

1. What Is Medical Inflation?

Medical inflation refers to the rate at which medical services and related costs rise. International consultancy Mercer Marsh Benefits, in its Health Trends 2025 report, defines medical inflation as "a subset of inflation that specifically relates to the rising costs of healthcare services and products only, such as medical procedures and pharmaceutical supplies"[¹].

Importantly, medical inflation does not move in step with the general Consumer Price Index (CPI). It is made up of three primary components:

- Price: doctor consultation fees, drug procurement costs, and hospital daily rates themselves adjusting upward;

- Utilisation: more medical services consumed per capita, including new tests and treatment cycles;

- Treatment evolution: new drugs, technologies and protocols displacing older (and usually less expensive) ones.

When all three rise simultaneously, medical inflation outpaces general inflation. In Mercer Marsh Benefits' 2025 report, Asia's overall medical inflation rate reached 13% — more than five times the region's general inflation[¹].

Why Does Medical Inflation Compound So Aggressively?

A simple illustration: if you save HK$10,000 a year at a 3% annual return, after 30 years the principal-and-interest is about HK$24,273. But if you needed to spend HK$10,000 a year on a medical item that itself grew at 8% per year, after 30 years that same item costs HK$100,627 — more than 10x.

This is compound growth on the spending side. When medical inflation stays elevated year after year, purchasing power erodes, and insurers must lift premiums simply to match actual claims experience.

2. How Severe Is Hong Kong's Medical Inflation?

Industry uses three major international insurance consultancies' annual surveys as the standard benchmarks:

1. AON, 2025 Global Medical Trend Rates Report: forecasts global medical inflation at 10% in 2025 — the third double-digit year of the past decade. Hong Kong's 2025 medical inflation rate is cited at 9.8%[²].

2. WTW (Willis Towers Watson), 2026 Global Medical Trends Survey: based on responses from 348 leading health insurers across 75 countries, the survey forecasts Hong Kong's 2026 medical insurance cost increase at 9.9%, with the broader Asia Pacific average reaching 14%[³].

3. Mercer Marsh Benefits, Health Trends 2025: based on a survey of 225 insurers across 55 countries (including 77 in Asia), found that more than half of markets had medical inflation rates above 10% in 2024–2025, with Asia at 13% overall[¹].

By comparison, Hong Kong's Composite CPI (published by the Census and Statistics Department) has run between roughly 1.5% and 3% in recent years. In other words, medical inflation in Hong Kong has consistently run three to five times faster than general inflation.

More importantly, this gap is not a short-term aberration. Mercer projects elevated medical inflation to persist at least through 2026 and likely beyond[¹][³].

3. Why Is Hong Kong Particularly Exposed?

Hong Kong's medical inflation profile is not accidental — it stems from several stacked structural drivers:

3.1 Heavy Reliance on Private Healthcare

Hong Kong runs a dual public-private healthcare system. Public hospitals (under the Hospital Authority) deliver universal but long-wait care; private hospitals offer faster, more flexible service at dramatically higher cost.

As of the rate schedule effective 1 May 2026 at Hong Kong Adventist Hospital — Stubbs Road (HKAH), daily room rates are: Standard ward (3–4 beds) HK$900, Semi-Private (2 beds) HK$2,300, Private (single) HK$3,400–HK$3,900, VIP suite HK$9,000, and Intensive Care Unit HK$10,000 per day[⁴].

Room rates alone reflect the high baseline cost of private care. Any hospital stay involving surgery, anaesthesia, drugs and equipment use easily runs into six-figure totals.

3.2 An Aging Population

According to the Legislative Council Research Office's brief ISSH32/2024, Hong Kong's population aged 65+ grew from about 600,000 in 1997 to 1.68 million in 2023 — 22.4% of the total population — and is projected to reach 2.3 million (29.1%) by 2033[⁵].

An aging population drives medical demand directly. As WTW notes, Hong Kong has "the highest life expectancy in the world" according to UN Vital Statistics, and an aging population combined with rising cancer incidence continues to push local medical inflation higher[³].

3.3 Imported Drug Costs

The vast majority of prescription drugs used in Hong Kong are imported. Drug prices are exposed to international supply, exchange rate, and patent protection effects. New-generation cancer immunotherapies, biologics and rare-disease drugs cost hundreds of thousands of HKD per treatment cycle — multiple times the cost of traditional chemotherapy.

Mercer notes that globally, cancer treatment has become the single largest category of insurance claim payouts[¹].

3.4 Specialist Fee Inflation

As the public-private quality gap widens, specialists migrate from public hospitals to the private market. Combined with sustained private-sector demand, specialist consultation and surgical fees adjust faster than general inflation. Cigna Hong Kong's consumer-education page notes that one of the main drivers of medical inflation is healthcare providers "regularly reviewing and adjusting their fees"[⁶].

Image: Unsplash / photographer Vitaly Gariev (@silverkblack), free to use under the Unsplash License.

4. What This Means for Your Retirement Plan

Back to the opening example: an FWD vBooster (F00069, HK$16,000 deductible variant) policyholder who buys in at 35 sees their official-table premium reach HK$42,091 at age 75. But because Hong Kong's life expectancy is around 85, the projection must extend at least that far — and from 75 to 85 the premium jumps again to HK$57,966; at age 90 it reaches HK$64,294. Roughly a 10x climb over 50 years. And that's only the age-band effect.

Layer on medical inflation (insurers periodically reprice the whole table) and the real-world premium climb is materially steeper. Below is a simplified illustration, for explanation only:

| Age | Official premium table (FWD F00069, today's rates) | + 2.5% annual inflation (conservative estimate) |

|---|---|---|

| 35 | HK$5,736 | HK$5,736 |

| 45 | HK$7,752 | about HK$9,900 |

| 55 | HK$12,038 | about HK$19,700 |

| 65 | HK$25,795 | about HK$54,100 |

| 75 | HK$42,091 | about HK$113,000 |

| 85 | HK$57,966 | about HK$199,000 |

| 90 | HK$64,294 | about HK$250,000 |

Source: FWD vBooster Medical Plan premium table dated 2 February 2026, held in VHISGuide's internal database. The inflated column is the author's hypothetical projection assuming a 2.5% annual medical inflation rate — a conservative estimate well below the 9–13% actual rates reported by Mercer / AON / WTW — and intended for illustration only, not an actual insurer forecast.

It's worth stressing: 2.5% is a deliberately conservative assumption — the three major consulting firms have observed actual medical inflation of 9% to 13% in recent years. Even on this far-lower-than-reality basis, by age 85 premiums already exceed today's level by 30x or more — the direction is not in dispute. Notice one thing: on the official table alone, premiums grow from HK$5,736 at age 35 to HK$42,091 at age 75 — about 7.3x over 40 years; but from 75 to 85, just one extra decade, adds another HK$15,875 of age-band step. Stopping the projection at age 75 quietly skips the steepest segment of the entire curve.

5. The "No-Coverage-in-Old-Age" Trap

Hong Kong's high life expectancy is exactly why this trap is bigger here than in markets with shorter post-retirement windows. The longer you live, the more years you need coverage AND the steeper the relevant segment of the premium curve becomes. In markets with shorter life expectancies, fewer policyholders ever reach the vertical-climb portion of the curve; in Hong Kong, nearly every 35-year-old enrollee will eventually face annual premiums exceeding HK$100,000 in their 80s.

And the trap is widening, not narrowing. Life expectancy keeps rising; medical inflation keeps compounding; the gap between the retirement-stage premium curve and the post-income window is structurally getting worse for each successive cohort. Today's 35-year-old faces a steeper version of the same problem their parents faced — not a milder one.

A significant share of Hong Kong's 60+ population doesn't drop their medical insurance because they no longer need it. They drop it because they can no longer afford it. When premiums climb from a few thousand HKD a year to one or two hundred thousand — while employment income has likely tapered or stopped — medical coverage becomes the cruel commodity that is most needed at exactly the moment it is least affordable.

The core problem: the premium curve and the income curve do not move in sync.

- Income curve: typically rises from age 25, peaks around 40–50, declines sharply from 60, and flattens after retirement at 65;

- Premium curve: rises gently from 35, steepens visibly from 55, and enters a "vertical climb" phase from 65 onward.

When the two curves cross, the problem appears: at the exact moment medical coverage is most critical, the premium also takes the largest bite from disposable income. Without prior preparation, only three paths remain: downgrade (drop to a lower-tier plan), switch (move to a cheaper option, but face fresh underwriting), or surrender (lose coverage entirely).

A surrender, in practice, means falling back fully on public healthcare — but public-sector wait times were exactly the reason most consumers wanted private medical coverage in the first place.

Hong Kong's Consumer Council, in its 2019 study Creating Sustainable Value for Private Health Insurance Market in Hong Kong, recognised this structural issue. The report documents a case of a 67-year-old whose annual premium more than doubled between 2013 and 2017 to HK$42,880 — with the insurer citing "enhanced benefits" and "medical cost inflation" as justifications[⁷]. The Council recommended that the industry provide policyholders with clearer per-age-band premium adjustment data, and consider raising entry-age limits to widen elderly access to coverage[⁷].

6. How to Prepare: Three Reasonable Paths

If you are between 30 and 55 today, with stable income, and starting to think seriously about retirement, the three paths below each play a different role and are not interchangeable: Path 1 addresses whether you can get coverage at all (insurability); Path 2 addresses where the money to pay for that coverage comes from (funding structure); Path 3 softens the marginal cost of that coverage (tax). They complement each other — this is not a three-way pick-one. Among the three, the one that actually addresses the 50-year premium curve as a structural problem is Path 2.

In other words: doing Path 1 alone secures your seat but doesn't guarantee you can afford the ride. Doing Path 3 alone saves on tax but doesn't solve the post-retirement cash-flow gap. The paths work properly only in combination.

Path 1: Enrol Early to Secure Your Insurability

This path is often misunderstood as "locking in a lower premium." In fact, every VHIS-certified plan reprices each year against your current age band — a 35-year-old who enrols today will pay roughly the same premium at age 50 as a 50-year-old who enrols at 50. Early enrolment does not lock in a lower long-run cost.

The genuine structural advantage of buying early is preserving your insurability. While you are young and healthy, you can typically be underwritten at standard rates. Once you develop a chronic condition in mid-life — hypertension, diabetes, thyroid issues, cardiovascular disease — re-enrolment can mean a 50–100% premium loading, specific exclusion endorsements, or outright decline. In other words, buying early solves the question of whether you have coverage, not how much that coverage costs.

Back to this article's central theme: early enrolment is a necessary prerequisite, not a standalone solution to the affordability problem at retirement. To actually address the 50-year premium curve, you still need the next two paths.

Use VHISGuide's Smart Filter to start from coverage needs and compare suitable plans across insurers.

Path 2: Build a Medical Reserve to Pre-Fund Future Premiums (the structural core)

If Path 1 secures your seat, Path 2 is about preparing the money you will actually need to pay. This is the only one of the three paths that directly addresses the 50-year premium curve as a structural problem: during the middle-age years when income is still in its upward phase, you compound today's savings into a pool that will cover the very high premiums of the post-retirement decades.

If you anticipate maintaining a high-tier medical plan (Semi-Private or Private ward) into your 60s and beyond, consider building a dedicated "medical reserve pool" — capital earmarked for future premiums and out-of-pocket medical expenses.

The reserve can be built from different categories of instruments, each playing a different role:

- Long-horizon compounding assets — for example, participating savings policies, savings-type whole life insurance, Qualifying Deferred Annuity Policies (QDAP). Stable expected returns, some with guaranteed components; suitable as the core stable layer with full compounding effect;

- Conservative fixed-income holdings — for example, time deposits, bond funds, government retail bonds. Higher liquidity, used to absorb short-term volatility and large self-funded medical events;

- Long-term growth investments — for example, index funds, diversified equity portfolios. Higher expected returns with higher volatility; used as a growth layer to raise the long-run return of the overall portfolio.

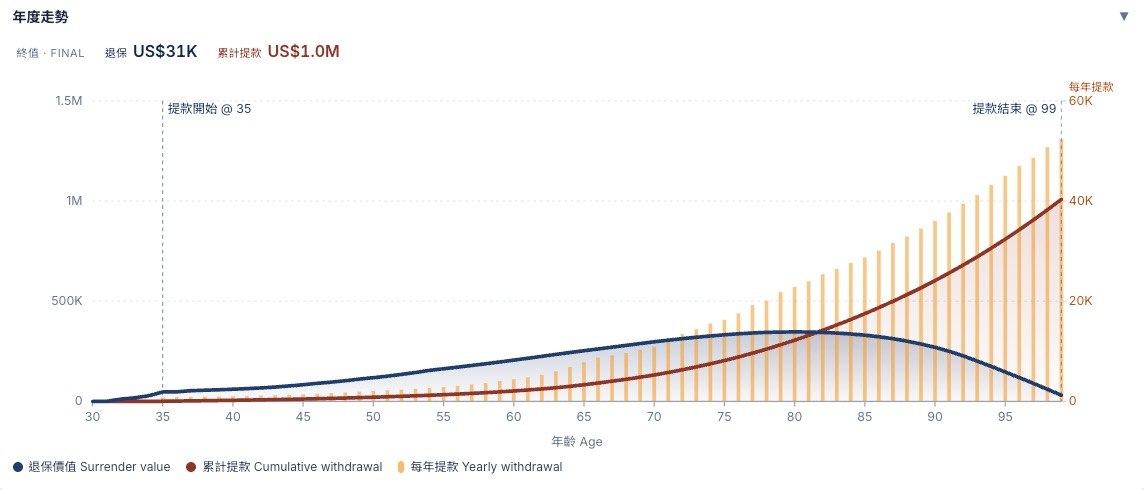

Illustration: a participating savings policy accumulates from age 30, with withdrawals starting at 35 to fund medical expenses (annual withdrawal = amber bars); the blue curve is surrender value, the red curve is cumulative withdrawals. A long-horizon asset can be drawn down while the underlying surrender value continues to compound — the core mechanism behind a medical reserve pool.

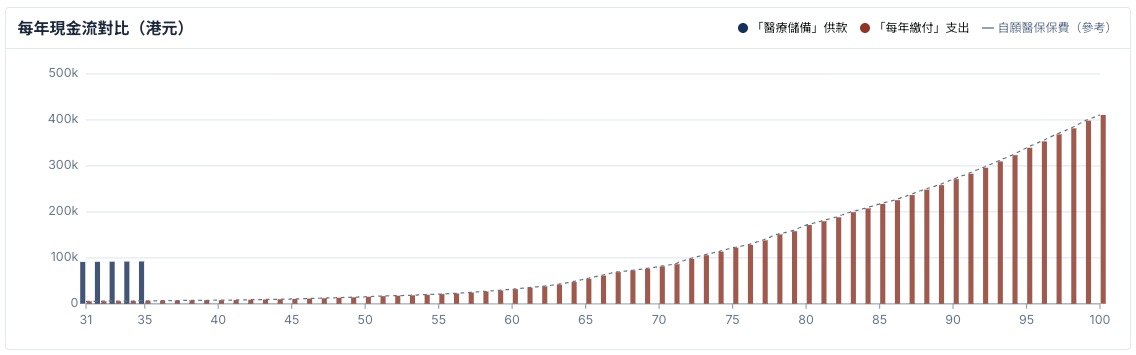

Illustration: blue = 5 years of concentrated saving across ages 31-35 (about HK$80,000-90,000 per year); red = the same person paying VHIS premiums year-by-year from age 35 all the way to age 100. Both cover an identical lifetime medical exposure, but the front-loaded path trades 5 years of focused contribution for decades of later cash-flow freedom.

Illustration: the cost of delaying contributions (illustrated using a USD-denominated savings policy). To hit the same target reserve, starting at age 30 costs USD$54,350 in total; delaying to 35 raises the cost by 31%; delaying to 45 raises it by 122%. The time-cost of compounding is not linear — it is asymmetric and accelerates fast.

When choosing a participating savings policy as the core layer, the earlier you start, the longer the compounding window and the higher the eventual withdrawal value. There are many participating savings products available in the market; expected returns, guarantee ratios, charges, and withdrawal flexibility differ materially between products and need to be compared on an individual basis. This article does not endorse any specific product.

How much to save and which product mix to use are best worked out individually with a licensed insurance intermediary or financial planner, based on your cash flow, risk tolerance and retirement goals.

Image: Unsplash / photographer Katie Harp, free to use under the Unsplash License.

Path 3: Maximise the VHIS Tax Deduction to Turn "Mandatory Cost" into a Tax Tool

Since the 2019/20 year of assessment, the Inland Revenue Department has allowed VHIS-certified plan premiums to be deducted from salaries tax, capped at HK$8,000 per insured person per year (covering the taxpayer themselves, spouse, children and specified relatives)[⁸].

According to Legislative Council written reply LCQ5 of 4 December 2024, in the 2022/23 year of assessment, around 404,000 taxpayers claimed VHIS premium deductions totalling about HK$2.987 billion, with around 74% of insured persons achieving the full HK$8,000 deduction[⁹].

In other words: if you pay tax, your VHIS premium's effective cost can be lower than its face value. At a 17% marginal tax rate, every HK$8,000 in premium costs you about HK$6,640 after deduction; for a family of four insureds, deducting up to HK$32,000 saves about HK$5,440 a year at the same marginal rate.

For full tax rules and filing details, see VHISGuide's Tax Guide.

7. Gifting Your Child a Lifetime Medical Reserve

The paths above all centre on one question: "What can a 35-year-old do for themselves?" But the time × compounding formula has an even stronger expression: a parent building a medical reserve in their child's name, starting from the child's birth or early years.

Consider the same child arriving at age 65, and ask how large their medical reserve is:

- Scenario A: parent does not intervene; the child begins saving on their own at age 35 — 30 years of compounding;

- Scenario B: at the child's age 0, parents take out a participating savings policy in the child's name and pay premiums for the next 10–20 years — 65 years of compounding.

Total premiums paid across the two scenarios can be roughly similar, but because Scenario B has 30+ extra years of compounding, the reserve at the child's age 65 — under typical long-term participating-savings return assumptions — can be 2 to 4 times that of Scenario A. The exact multiple depends on the policy's dividend fulfilment ratio; the figure here is illustrative. In other words, the 50-year premium curve the child will face later in life is supported by a substantially larger reserve.

Why "Parents Aged 30 to 45" Is the Most Suitable Payment Window

Parents in their 30s and 40s are typically at the peak of their earning years. Shouldering 10–20 years of premium payments during this window is far more feasible than asking the child — who at age 35 is often juggling a mortgage, young family, and their own household expenses — to fund the same reserve themselves. It is an inter-generational allocation of effort: parents pay during their highest-earning phase, and the child enters their retirement-planning years already holding a fully-formed reserve that can fund their own future medical premiums.

Twin Advantages: Underwriting and Tax

A participating savings policy on a newborn or young child sits at the lightest possible point of that person's lifetime underwriting curve. Locking in standard-rate coverage before any medical history exists protects the child from future loadings, exclusions or declines tied to conditions acquired later in life.

Separately, where parents also take out a VHIS-certified plan on the child and pay the premium themselves, the IRD allows the parent to claim that premium under their salaries-tax deduction, capped at HK$8,000 per insured person per year[⁸]. The parent's "gift," in tax terms, is partially returned.

A Trade-off That Must Be Stated Clearly

Participating savings policies are not free of friction. Their structural limitations include: low surrender values in the early years, restricted cash-flow liquidity, a split between guaranteed and non-guaranteed components that varies by product, and a dividend fulfilment ratio that has not historically delivered 100% every year — actual realisation varies materially by insurer, policy vintage and market environment. This article does not present any single instrument as "the answer." Treat it as one tool within a wider medical-reserve portfolio, used alongside other asset categories.

How many years to fund, and which product category to choose, depend on the parents' cash flow, the child's long-term needs, and the historical dividend fulfilment ratios of different insurers — best assessed individually with a licensed insurance intermediary or financial planner.

For a newborn child, the most valuable gift may not be a branded toy or an education fund — it may be a reserve pool that travels alongside them through sixty, seventy, even eighty years of medical coverage. The power of compounding is shown most fully when the starting point is set as early as possible.

8. Frequently Asked Questions (FAQ)

Q1: Why does medical inflation differ so much from general inflation?

General inflation (CPI) reflects the prices of everyday consumer goods, with heavy weight on food, housing and transport. Medical inflation reflects the price of medical services and products — a basket pushed by three additive forces: pure price rises, higher per-capita utilisation, and treatment evolution (new drugs/technologies replacing older ones). The "treatment evolution" component has no real counterpart in the CPI basket. Add in demographic-driven demand from aging, and medical inflation will structurally outrun general CPI.

Q2: Can insurers raise premiums without limit?

VHIS-certified plan premiums are governed by the VHIS regulatory framework and the Insurance Authority. Insurers cannot unilaterally reprice an individual policyholder based on that individual's claims (i.e. no individual repricing); they may only adjust the premium table on the basis of overall portfolio claims experience, applying fair and reasonable principles. The IA has also conducted market reviews on medical insurance pricing. That said, for an individual policyholder, age-band stepping plus periodic full-table repricing produce a real, long-term upward trajectory.

Q3: What if I can't afford the premium after a sharp increase?

Three common workarounds: (1) downgrade within the same insurer to a lower-tier plan (e.g. from Private to Semi-Private, or Semi-Private to Standard ward); (2) increase the deductible to reduce the premium (e.g. switch from HK$0 deductible to HK$25,000 or HK$50,000 deductible); (3) maintain a VHIS Standard plan within the same insurer as a minimum baseline. Which option is most cost-effective depends on personal health, other assets, and family medical-expense arrangements — work the numbers individually. Note: whether any of these three moves (downgrade, deductible increase, plan switch) requires fresh health underwriting depends on the insurer's policy, plan type, and your enrolment history — not every adjustment triggers a full underwriting review. Before making any change, ask the insurer or a licensed intermediary about the current underwriting requirements for that specific plan.

Q4: Is annual premium increase the same across all insurers?

All VHIS-certified plans price by age band, so every VHIS plan rises with age — that is structural, not insurer-specific. But the steepness of the premium curve differs across insurers: some have markedly steeper curves in the 55–75 band; others are flatter. Before enrolling, check the full premium ladder of any plan via the VHISGuide comparison tool.

Q5: Besides VHIS, what else can hedge medical inflation?

Common complements include: (1) building a medical reserve pool (par savings + fixed deposits); (2) MPF Tax-deductible Voluntary Contributions (TVC) and Qualifying Deferred Annuity Policies (QDAP) — both eligible for up to HK$60,000 combined annual tax deduction, useful as long-horizon retirement capital; (3) sustained investment to grow the underlying asset base, so that even higher premiums at retirement can be funded from total assets. No single best answer — the three paths usually combine.

Q6: Why is buying early so much more cost-efficient than buying late?

Two reasons. First, preserving insurability — while you are young and healthy, you can typically be underwritten at standard rates, avoiding future 50–100% premium loadings, specific exclusion endorsements, or outright decline once you develop conditions like hypertension, diabetes, cardiovascular disease or other chronic illness. Note that buying early does not lock in a lower long-run premium: every VHIS plan reprices each year against your current age band, so a 35-year-old enrolee will pay roughly the same premium at age 50 as someone who only enrols at 50. Early enrolment addresses the question of whether you can get coverage, not how much it costs.

Second, a longer compounding window — if you simultaneously build a medical reserve (see Path 2 in the main article), starting 10 years earlier produces a materially larger principal. Hong Kong's average life expectancy is around 85 and still rising; that reserve has to last longer than most people assume. The arithmetic of compound growth means every additional year of head start translates into a meaningfully larger pool available in your 80s and 90s.

Q7: Is VHIS alone enough to cover retirement medical costs?

VHIS covers inpatient, surgical and related treatment costs. But retirement medical spending also includes: (1) outpatient and chronic-disease medication (VHIS generally doesn't cover); (2) long-term care (nursing homes, home care); (3) dental routine care (VHIS Standard excludes); (4) discretionary wellness spending. VHIS alone is therefore not enough for full retirement medical coverage. The recommendation is to treat VHIS as a core layer and pair it with a medical reserve pool and other healthcare-spending planning.

9. Further Reading

Internal Tools and Guides

- Smart Filter — start from coverage needs and compare suitable VHIS plans across insurers

- VHIS Tax Guide — detailed rules and filing instructions for VHIS premium deductions

- Insurer Directory — Hong Kong's VHIS-certified insurers and their product ladders

Authoritative External Sources

- Voluntary Health Insurance Scheme — Hong Kong SAR Government official site — VHIS statutory information, certified plan list, template terms

- Hong Kong Insurance Authority (IA) — insurance industry statistics, market review announcements

- Hospital Authority Annual Reports — public-sector healthcare operating and financial data

- Census and Statistics Department — demographic and CPI baseline statistics

Citations

[¹] Mercer Marsh Benefits, Health Trends 2025 (survey of 225 insurers across 55 countries, including 77 in Asia), published December 2024. https://www.mercer.com/en-hk/insights/total-rewards/employee-benefits-optimization/mmb-health-trends/

[²] AON, 2025 Global Medical Trend Rates Report, published December 2024. Hong Kong 2025 medical trend rate: 9.8%; global average: 10%. https://www.aon.com/en/insights/reports/the-global-medical-trend-rates-report

[³] WTW Willis Towers Watson, 2026 Global Medical Trends Survey (based on responses from 348 leading health insurers across 75 countries), published October–November 2025. Hong Kong 2026 medical inflation forecast: 9.9%; Asia Pacific: 14%. https://www.wtwco.com/en-hk/news/2025/11/double-digit-medical-cost-increases-projected-to-persisit-into-2026-and-beyond-in-asia-pacific

[⁴] Hong Kong Adventist Hospital — Stubbs Road, Daily Room Rates, effective 1 May 2026. https://www.hkah.org.hk/en/fees-and-charges/facilities/daily-room-rates

[⁵] Legislative Council Research Office, ISSH32/2024: Elderly population in Hong Kong, published 10 December 2024. https://app7.legco.gov.hk/rpdb/en/uploads/2024/ISSH/ISSH32_2024_20241210_en.pdf

[⁶] Cigna Hong Kong, "How does medical inflation affect premiums?" consumer education page (2024). https://www.cigna.com.hk/campaign/know-health/en/medical-inflation-in-hong-kong

[⁷] Hong Kong SAR Consumer Council, Creating Sustainable Value for Private Health Insurance Market in Hong Kong, published 29 May 2019. https://www.consumer.org.hk/f/initiative_detail/301160/Medical_Insurance_Report_Final_v2.pdf

[⁸] Hong Kong Inland Revenue Department, Tax Deduction for Qualifying Premiums Paid under the Voluntary Health Insurance Scheme Policy, applicable to the 2024/25 year of assessment; cap of HK$8,000 per insured person per year. https://www.ird.gov.hk/eng/tax/ind_vhis.htm

[⁹] Hong Kong SAR Government Information Services, LCQ5: Voluntary Health Insurance Scheme (Legislative Council written reply, 4 December 2024). VHIS certified-plan policies as at 31 March 2024: approximately 1.34 million; 2022/23 year of assessment: 404,000 taxpayers claimed VHIS deductions. https://www.info.gov.hk/gia/general/202412/04/P2024120400321.htm

[¹⁰] Hong Kong SAR Centre for Health Protection, "Life expectancy at birth, 1971 - 2024". 2024 life expectancy at birth: 82.7 years for males, 88.2 years for females. https://www.chp.gov.hk/en/statistics/data/10/27/111.html

FWD vBooster Medical Plan premium table: drawn from VHISGuide's internal database, corresponding to FWD certified plan F00069 (vBooster Medical Plan, HK$16,000 deductible variant), premium effective date 2 February 2026. Age 35 non-smoker annual premium HK$5,736; age 45 HK$7,752; age 55 HK$12,038; age 65 HK$25,795; age 75 HK$42,091; age 85 HK$57,966; age 90 HK$64,294. See also the FWD premium ladder for the full plan series.

This article is provided for education and reference only and does not constitute insurance, tax, or financial advice. Cited data should always be verified against original sources. Before enrolling in any VHIS plan, please carefully read the plan's Principal Brochure, Exclusions and Premium Table, and consider professional advice based on your individual circumstances.